FIVE STAR CUSTOMER SERVICE!

FIVE STAR CUSTOMER SERVICE!  +1 866 921 8890

+1 866 921 8890

A rental property creates an extra income stream for investors. Buying rental properties requires significant funding that may not be within your reach. Fortunately, prospective property owners can access a rental property mortgage to acquire a rental property in Ontario.

Qualifying for a mortgage on a rental property is typically hard, thanks to the stringent requirements imposed by many lenders. Owning property is one of the best financial decisions you’ll ever make.

Understanding the requirements to qualify for a mortgage in Ontario can help you make informed choices. This guide explores everything you need to know about getting a mortgage for a rental property in Ontario.

Definition of a Rental Property

Potential property owners must understand all the aspects of property mortgages to be adequately prepared for the mortgage application process. So, what is a rental property? A rental property refers to real estate purchased by a person (investor) for leasing or renting out.

Investors buy property for two main reasons:

- Generating rental or lease income, and

- Making a profit in the form of capital gains when appreciated property is sold.

There are two main types of rental properties: residential and commercial rental properties. Each type can be acquired with the help of mortgage broker Toronto and has pros and cons, so you should carefully consider your investment goals to determine the ideal option that matches your specific needs.

Residential rentals are properties bought and leased or rented out by property owners—landlords, to tenants. To be classified as residential property, the land where the property stands should have been specifically zoned for residential rentals. Common residential rental properties include:

- Single-family homes

- Townhomes and condos

- Apartment complexes

Residential rental property owners use rental or lease income to service their mortgages. In other words, mortgages for rental properties aren’t serviced out-of-pocket by property owners in many cases.

Sometimes rental income is not sufficient to service the mortgage and cater to property maintenance expenses. In such cases, property owners have to look for extra ways of servicing their mortgages.

Unlike residential rentals, the occupants of commercial rental properties are businesses and not tenants. Mortgages for commercial properties typically attract stricter conditions and higher costs of financing—interest rates. Common types of commercial rental properties include:

- Office buildings

- Buildings housing retail stores

- Industrial buildings

Do you wonder why many people prefer mortgages over cash payments when buying property, even when they can afford it? Unlike buying property on cash terms, mortgages allow investors to own property with other people’s money.

Eligibility for a property mortgage can vary by financiers. For instance, some lenders limit the number of houses you can buy on a mortgage. Others don’t have such limitations, so you must consider all the conditions imposed by a lender when applying for a mortgage.

The consequences of getting a rental property mortgage involve more than servicing the loan. Other expenses will automatically come up, including property taxes, fees, and more, whether your tenants submit rent or default.

As a minimum requirement, your financiers will expect you to service the mortgage regardless of changing conditions. That said, you must do everything within your power to fulfill your end of the bargain.

Mortgage Process For a Rental Property in Ontario

Eligibility Requirements

1. Credit Score

How hard is it to get a mortgage for an investment property? Lenders use your credit score to determine your eligibility for a property mortgage in Ontario. These requirements can be stringent owing to the risk involved. However, some lenders are flexible, so you should do a background check before securing a mortgage facility.

The bottom line is that mortgage applicants must guarantee their financiers that they have the means to service their mortgages without defaulting. Besides a credit rating, you must meet the following conditions to secure a rental property mortgage in Ontario:

- Sufficient rental income to service your loan

- A debt-to-income ratio of 1.1 or more

- A minimum and maximum mortgage down payment of 5% and 20%, respectively, and more

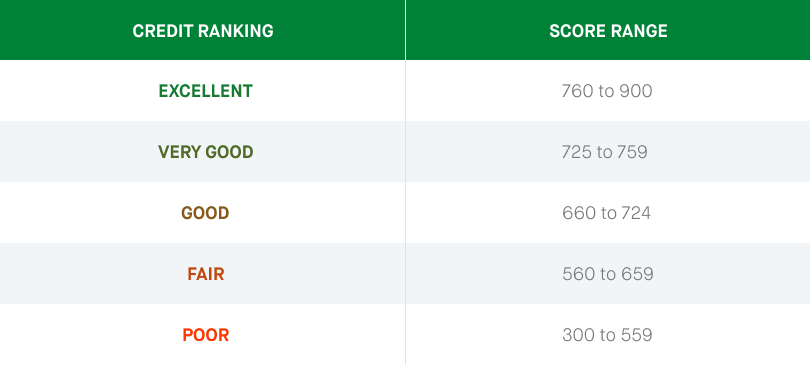

A credit score is a measure of creditworthiness, also known as credit rating. Credit score typically ranges between 300 and 850, so the credit rating required by different lenders can vary.

The upper extremity of the above range denotes high creditworthiness, while the lower extremity signifies low creditworthiness. Your credit score can impact numerous aspects of a mortgage, including:

- Approval,

- Interest rate, and

- The mortgage type you qualify for, among others.

A good credit rating improves the chances of negotiating a good rental property mortgage plan. Many Ontario mortgage lenders require applicants to have a minimum credit score of 600.

2. Income

Expected rental income is a major factor that influences your eligibility for a rental property mortgage. Any financier would want to know if the projected rental income will sufficiently service your mortgage realistically and sustainably.

Taking a mortgage doesn’t eliminate your other financial obligations—you’ll still have bills and other daily expenses. That said, reviewing your projected rental income will help your financiers make informed choices.

Gross rental income can be equated to business revenue. In other words, it’s the net income generated by your property owners without factoring in expenses.

Gross rental income is a product of monthly rent per unit and the total number of occupied units. Lenders typically base their calculations on annual rental income. They also factor in the vacancy rate when calculating annual rental income.

The vacancy rate eliminates the idle time or the time your rentals won’t be generating income from the equation. So, your annual net rental income should be calculated as follows:

Gross Rental Income = Monthly Rent * 12 months * (1 – [Vacancy Rate÷100])

It’s time to determine your net annual rental income after calculating the gross rental income. Net income is what you get after deducting all costs or expenses associated with your property, including:

- Maintenance expenses

- Repair expenses

- Property tax

- Salaries and wages for caretakers, and more

A rental property income calculator can capture all elements that impact rental income, including those not listed above. Mortgage lenders use two approaches when calculating rental income— cash flow and appreciation approaches.

The cash flow approach is based on the rental income formula (above). On the other hand, the appreciation method is based on capital gains, calculated as follows:

Capital Gains = Prevailing market price less Net Value of Your Property.

3. Debt-to-income ratio

The debt-to-income (DTI) refers to the percentage of gross monthly income dedicated to the payment of debts. Debt-to-income and Debt Service Coverage (DSCR) ratios are very similar but have a slight difference. DTI is typically used in all other industries except the real estate market. DSCR is specifically for the real estate industry.

DSCR is based on personal income for residential properties. On the other hand, this ratio is based on rental income for commercial rental properties. Lenders use DSCR to determine lending, or rather, borrowing risk. The debt Service Coverage Ratio is calculated as follows:

DSCR= Net operating income / (Monthly mortgage repayment * 12)

Lenders require applicants to have a minimum debt service coverage ratio of 1.1 to qualify for a mortgage. The higher your DSCR, the better.

4. Down payment

A property down payment is the percentage of a mortgage prospective property owners must pay upfront. Your down payment is the initial investment for the property in question. Down payment can vary by case because each case is affected by different factors.

People who haven’t resided in the subject property for at least one year require a 20% down payment. Prospective property owners who comply with the Canada Mortgage and Housing Corporation’s minimum requirements can access better down payment rates of between 5% to 10%. The current CMHC requirements are:

- Minimum credit rating of 600,

- Debt service coverage ratio of 39% for GDS and 44% for TDs, and

- The down payment must be paid by mortgage applicants.

Down payment is calculated as follows if you comply with the CMHC requirements:

- 5% for the first $500,000, and

- 10% for values between $500,000 and $1,000,000.

5. Amortization Period

Amortization period or term refers to the mortgage repayment period if made in regular intervals. In the context of rental property mortgage, amortization refers to how much time you take to fully settle your property loan.

Many prospective landlords prefer longer amortization periods to reduce the monthly repayment amounts or monthly interest expenses. The more the amortization period, the less the payable mortgage interest, meaning more profits.

Many lenders offer maximum amortizations of anywhere between 25 and 35 years for residentials. Maximum amortization (35 years) is only for people with CMHC mortgage insurance with a down payment of less than 20%.

The maximum amortization period is 35 years if the down payment is more than 20% and living in the subject property is not a precondition. The downside of a longer amortization is that it attracts an amortization extension fee and higher interest rates.

Shorter amortization periods attract higher regular repayment amounts. On the other hand, longer amortization periods spread the regular repayments over an extended time. So, it’s important to understand how amortization can impact your finances to make informed choices.

Closing Costs

Common Type of Closing Costs

Legal Fees

Closing costs (which form 3% to 4% of the property value) include legal and other expenses like transfer tax and inspection fee. Legal fee and other closing costs are typically paid upfront by prospective property owners in Canada.

By law, you must have legal representation when buying or mortgaging property in Ontario. The average legal fee for property lawyers can range from $500 to $1,500.

The applicable legal fee depends on many factors. These factors include the complexity of the assignment, jurisdiction and your negotiating skills, among others.

Land Transfer Tax

A real estate transfer tax, also known as a deed transfer tax, is a one-time fee payable when transferring property ownership to a buyer or heir (in estates).

Land transfer tax is payable to the government, and it’s considered an ad valorem tax. The receiving authority (where you should pay the tax) depends on where you live. It can either be the provincial government or the municipality.

In simple terms, land transfer taxes are based on the assessed value of a property. Calculating the applicable tax for your property is not always easy. Fortunately, you can use a Land Transfer Tax calculator. Land transfer tax must be paid for any property that requires a title to prove ownership when changing hands.

Transfer taxes are mandatory under all property deeds and the numerous legal documents involved in property transactions. Canadians living in Ontario, British Columbia, and Prince Edward Island are eligible for land transfer tax rebates.

A rebate is a refund for excess tax payment (land transfer tax in this case). “Rebate” and “discount” are often confused, but they’re distinct. While a discount reduces your liability, a rebate doesn’t.

Tips to Successfully Get a Mortgage for Rental Property in Ontario

Go Through the Main Methods For Mortgage Approval

Qualifying for a rental property mortgage, the world over, depends on your creditworthiness, as aforementioned. This section shares tips to get a mortgage for a rental property in Ontario successfully.

Understanding the minimum requirements to qualify for a rental property mortgage in Ontario is the first step to preparing yourself. You can get the requirements online or by visiting their physical offices.

Seek clarification on everything about the mortgage in addition to the minimum requirements. Your mortgage for a rental property can be approved if you meet specific minimum conditions, including:

- Having a minimum credit score of 300 to 850

- Acquiring a property that can generate sufficient income to service the mortgage

- Having a debt service coverage ratio of 1.1 or more

- Having the capacity to settle the down payment, and

- Accepting the amortization offered by your financiers

Additionally, the target property must meet the following conditions:

- The value of the property must be above 1 million Canadian dollars

- The property should have a minimum of 4 units

- You should be residing in one of the units within the property

Getting a mortgage for a rental property may seem difficult, thanks to the strict minimum requirements imposed by lenders. However, you only need to fulfill the above-listed conditions to secure a rental property mortgage in Ontario.

Mortgage for Rental Property in Ontario – FAQs

How many units does the rental property have?

The number of units in your property can impact your eligibility for a rental property mortgage in Ontario. If the property has 1 to 4 units, it will be zoned residential or, rather, a small property.

Getting a mortgage, in this case, can be more challenging than with a property with over 4 units. Residential properties with 1 to 4 units can receive a maximum of 80% financing in Ontario.

On the other hand, properties with 5 or more units are typically zoned commercial. Consequently, qualifying for financing won’t be easy, but not impossible.

If you qualify for a mortgage with commercial properties, interest rates will likely be high. You will also have to look for financiers who offer mortgages for commercial properties, and they’re not many.

Is it going to be a profitable property?

No one will lend you money if they don’t believe in your investment ideas. That said, your lenders must evaluate the feasibility of your investment project. Generally, your rental property must be profitable to qualify for a rental property mortgage.

What’s considered a good investment can vary by a mortgage lender. However, many lenders use the total debt service ratio (TSDR) to make informed lending decisions. TSDR is calculated by dividing your total monthly expenses and total monthly income.

Formula:

TDSR= Total monthly expenses / Total monthly income from all sources

Many lenders require loan applicants to have a TDS ratio of 40% or less. Using the TDS ratio to determine your eligibility for a mortgage has one disadvantage, though. Lenders decide the portion of your rental income that should be used to calculate the TDS ratio.

Suppose your rental income is $1,000. You want the whole amount to be factored into the TDS ratio. Unfortunately, what matters is your lender’s allowable amount, which can be far much less than your rental income.

How many rental properties do you own in general?

The number of rental properties you own can impact your eligibility for a rental property mortgage. As you accrue more property, lenders will likely limit the number of properties you can use to determine rental income.

The total debt service (TDS) ratio measures the portion of your income that goes to servicing debts—a mortgage, in this case. Limiting the properties when calculating TDSR limits the chances of qualifying for a rental property mortgage.

Are you going to live in that rental property?

The property will be considered owner-occupied if you’ll be residing in one unit within the property. One advantage of owner-occupied properties is that you can access lower down payment rates of between 5% to 10%.

Your property will be zoned non-owner occupied if you won’t be living there, attracting higher mortgage down payment rates. While you may not love living in the property, you may want to reconsider your decision to enjoy lower down payment rates.

+1 866 921 8890

+1 866 921 8890