FIVE STAR CUSTOMER SERVICE!

FIVE STAR CUSTOMER SERVICE!  +1 866 921 8890

+1 866 921 8890

Bad Credit Mortgages

Toronto

Award Winning Customer Service To Each And Every Single Client!

Let's Get Started

Bad Credit Mortgage Broker – We Help With Mortgage for People With Bad Credit

Do You Need A Bad Credit Mortgage In Toronto?

Getting mortgage approvals in Canada has recently become more challenging because of the recent changes in mortgage regulations. It gets even harder to get mortgage loans for those who have bad credit and low income. Despite the challenges, you can still get a bad credit mortgage if you have a poor or no credit score in Canada. This type of mortgage isn’t usually available from traditional lenders, which means you’ll only get one from an alternative mortgage lender for people with bad credit. Large lending institutions insist on good or excellent credit scores before approving a mortgage, but that does not guarantee approval. They can still reject applications even when the applicant has a high credit score. Even so, a good credit score is still the only way to improve your chances of getting approved. Try to avoid behaviours that could reduce your score, such as missing credit card payments and failing to file taxes. Additional factors that can reduce your credit standing are arrears in taxes, many credit card debts, large balances on store cards, outstanding mortgages, and bankruptcy.

If your score lowers, the stringent policies and regulations surrounding conventional lenders, which are a concern for many borrowers, will hinder you from getting a mortgage from your bank. The policy changes have left unconventional lenders, also known as B lenders, as some of the only options. The other option for bruised credit mortgage is private lenders. Adrianov Mortgage brokers are here to help get you any type of mortgage you need. Our connection to numerous lenders in all the major cities of Canada makes it possible for us to give our clients a wide range of options, which makes it easier to get a suitable mortgage type, including bad credit mortgage. Most of the lenders we work with have experience with bad credit mortgages, which allows us to get you the right mortgage solutions with the best loan terms and lowest interest rates. Our mortgage brokers understand that life’s challenges can lower your credit score and prevent you from getting real considerations from lenders. We believe that you deserve the financial help you need even if you have failed to make timely payments in the past.

If you need the best bad credit mortgage broker in the market, Adrianov Mortgage is the place to look. To us, the financial bad luck you’re experiencing shouldn’t keep you from owning your home or making other investments. The private and alternative mortgage lenders for people with bad credit that we work with only pay attention to the property you have rather than your credit history. They want to know that your property has the right value, is at an ideal location, and is in the best condition for marketability. They would rather tie the risk they are taking with you to your property instead of your financial income. Because of this, they are the perfect solution for mortgages for people with bad credit or new residents of Canada. Our team can help you understand anything you want to know about bad credit mortgage Toronto lenders. We will give you all the information regarding the mortgage risk levels associated with your credit score and how to maneuver the bad credit loan systems.

What To Do When You Have Bad Credit?

Do You Have Poor Credit?

The common thought is that you can’t get a mortgage with poor credit. Lenders are reluctant to do business to people with bad credit history because it puts them at risk and there is a lack of trust. If you find yourself in the position of bad credit do not think that you are without options when it comes to getting a mortgage. It may take a little bit more patience and effort but with help from mortgage lenders for people with bad credit it is definitely possible.

We Know How To Go About Bad Credit Mortgage

Poor credit can be a huge hindrance when it comes to mortgages, but no matter the credit rating we always make sure to work out a specialized and individualized mortgage for our customers.

At Adrianov Mortgage we figure out a unique plan for every individual to get a good mortgage and that includes people with poor credit. We know how to go about such issues and find suitable options.

Getting A Mortgage With Bad Credit

As a self-employed person in Canada, one of the biggest problems you'll face is getting a mortgage even if you have a good score. However, having bad credit shouldn’t keep you from applying for any mortgage you want. You can still qualify for a mortgage with bad credit when you follow the right steps and hire a committed bad credit mortgage broker to handle your case. With these, it also becomes possible to get second or third mortgages before completing the first one. Our brokers in New Market are available to guide you through the processes and help you come up with a plan that eases your financial burden.

Your Income Record

With a bad credit mortgage, the focus will be on your ability to pay back the loan on time instead of your past failed payments. That is why your income capacity is essential. You need to prove to the lender that you can earn enough money to cover your monthly payments until the mortgage term is over. After viewing your records, the lender will determine the right amount to give you using Gross Debt Service Ratio or Total Debt Service Ratio. In most cases, bad credit mortgage lenders in Toronto will only approve applications for borrowers with less than 30% of the GDS and TDS. Try to keep your debt ratio as low as possible. If you can’t, try to get a down payment of at least 35%. Your bad credit mortgage broker can help you arrange all your essential proof of income documents, such as tax returns, and make sure they are up to date.

Large Down Payment

A large down payment reduces the mortgage you need to top up to the purchase price. If you don’t have good credit, you will need a larger amount of down payment to reduce the risks for the lender. The more you can pay on your own, the less they will have to lend you. If you can’t raise enough down payment, use one of your properties as cross collateral. Some mortgage lenders for people with bad credit even allow you to use a property from a family member or friend. The collateral properties will increase your loan to value ratio, which will reduce the lender’s risk tremendously. As a result, the lender will offer you lower interest rates and give you better payment terms. Adrianov Mortgage brokers is the easiest company to get a bad credit mortgage with, in all the major cities of Canada. Our brokers will make sure you meet the best lender for your bad credit situation.

Property Appraisal

An appraisal tells you the value of the property, after which you and the lender can determine the amount of bad credit mortgage you’re worth. That is why it is mandatory before any mortgage application. The appraisal should be done by a reputable professional. Some mortgage lenders for people with bad credit will request that the job be done by a company they have worked with before, while others will let you choose any appraisal company. Do at least two appraisals, even when the lender requests that it should be done by a specific company. You’ll be able to determine the average value and a more accurate result. When lenders find out the value of the property, they will be able to use that information to calculate the loan-to-value ratio and figure out the level of risk they should take with their money. Some of them can give you up to 90% of the property value, but most will give between 80% and 85%.

Co-Signer

Getting a mortgage with bad credit is also possible when you partner with other people. It could be your loved one or a business partner. A low credit score is enough to make any lender skeptical about giving out their money. A co-signer with a higher score than yours can reduce the risks for the lender and motivate them to give you the loan you need. Your co-signer should also have a higher income than you and should be willing to guarantee the loan. That means they should be willing to take the payment responsibility in case you default. There have been cases where co-signers have helped borrowers qualify for loans from conventional lenders. That shows that having one will increase your value and the chances of qualifying for a mortgage with bad credit. It doesn’t have to be a family member or a spouse; it can also be a friend or investment partner.

Employment Information

Since most bad credit mortgage lenders don’t focus on how you’ve handled your previous debts, they will rely on the stability of your income. They’ll need to know that you can earn enough salary for an extended period to cater to the mortgage payment. You will have to submit your T4 form to the lender to show your salary, gratuities, bonuses, vacation pays, and other wages you earn in the line of duty. Your payslips and other forms related to your additional income sources, such as investment ownerships, will also come in handy. Your freelance and rental income documents can also help show that you earn more and increase your bad credit mortgage range.

Information About Your Debts

Your existing debts will affect your ability to pay the new mortgage, and that is why they interest the lender. You will have to divulge all the information about the loans and bills you’re servicing by giving the lender all the relevant documents. Whether you’re paying off credit cards, student and personal loans, child support, spousal support, or car payments, your lender will want to know about them. Too many debts may not be a hindrance to your mortgage acquisition, especially if you have a high income to match it. However, you should still try to reduce them before your mortgage application to show the lender you’re responsible.

Mortgage Offers

...pick the one thats right for you.

Credit Card Ratings in Canada

Credit card ratings in Canada range from 300 to 900, and they are usually given by one of two main bureaus: Equifax and Transunion. Both bureaus can calculate credit scores using different methods, but their results are always similar. The ideal score for getting mortgage approval in Canada easily is 650. Higher scores than that will increase the chances of getting approved quickly, while a lower one will make it harder. The 650 mark is a fair score, and anything less than 600 is poor. You should always find out your score before any application because it can limit your negotiation power. You should also check your credit report and make payments at the appropriate time to improve it. Checking your credit information can help you prepare accordingly by showing you what you’ll likely qualify for. You will be able to budget accurately to avoid being overwhelmed by the mortgage payment and create an affordable payment plan.

At Adrianov Mortgage, we understand the crucial role of credit scores in a bad credit mortgage application process. We know the advantages of a higher credit card score, especially how it makes mortgage approval easier. We will give you all the tips to improve your credit rating and enroll you in the right programs to help you achieve the same. Our esteemed bad credit mortgage brokers focus on delivering customized services. We will analyze your financial situation and the factors that have led to a low credit rating before suggesting the correct solutions that will improve it. We will also get you the right mortgage lenders for people with bad credit depending on the rating you currently have, as we help you improve it for future lending. Whether you need a bad credit mortgage or a self-employed mortgage with good credit ratings, we will make sure you get it.

Excellent Credit Score (740-900)

To get such a score, you have to make timely payments, pay your debts in full, and use less than the credit limits you have. Such a score has a lot of benefits when you want to borrow. You will get faster approval, and your mortgage will come at lower rates. You will also get a higher limit and other premium benefits for your credit cards and mortgages. The loan options you can get with such a score are also endless. Both traditional and private lenders will have no problem giving you the mortgages you need, which means you won’t stand a chance of being rejected. An excellent score shows lenders that you are responsible and you practice good financial skills. They’ll know they can depend on you to pay the loan.

Good Credit Score (690-739)

Having a good credit score shows lenders that you are responsible for your finances, so you will have very little trouble getting the exact mortgage you want. To get that rating, you have to avoid making late payments or maximizing credit card limits. Some of the benefits you will experience with a good score are low-interest rates from banks and alternative lenders and easier approval processes. Most lenders also have reward programs for credit card users in the rating category. A good score also increases the types of lenders you can borrow from. Your bank will most likely consider giving you the money you need without too many restrictions. If not, you will find a private lender with the best terms.

Fair Credit Score (660-689)

This credit range is still a good one, but it won’t give you the same benefits as the other two categories above. You will have to pay slightly higher interest rates, and some of the traditional lenders may not give you real consideration. You get this rating if your credit report isn’t great. You may have made late payments regularly and may have gone overboard with your credit cards. Although having a fair score still gives you many borrowing options, lenders may not give you the chance to negotiate for better terms and rates. Your chances of getting unsecured loans from private lenders will be higher than getting secured loans from banks.

Poor Credit Score (570-649)

A poor credit score will make it harder for you to get mortgage approval from both alternative lenders and banks. It indicates that you can’t manage your payments properly, which lenders will see as high risk. If you manage to get a loan, it will come at a higher interest rate, which will increase your payments over the mortgage term. Additionally, you won’t be eligible for most mortgages and credit cards. If you have a poor credit score, it will be better to improve it before seeking a mortgage. Normalize paying your bills in time, and try not to have too many bank accounts. However, if you need the mortgage urgently, our mortgage brokers will help you explore ideal options that won’t be too costly to pay.

Bad Credit Score (300-569)

Very few lenders will consider giving loans to people who have credit scores that are lower than 500. To have this rating means you have continuously made poor financial choices, such as failing to pay debts on time. A bad credit score will remain in your credit report for as long as 7 years. During that time, getting any type of loan will be next to impossible. Adrianov Mortgage brokers can help you find a suitable mortgage lender for people with bad credit. We don’t discriminate against bad scores, and we understand that you can experience uncontrollable circumstances that damage your finances. We will help you improve your credit and get you the special lenders that deal with bad credit loans. Even though mortgages given to bad credit borrowers come at very high rates, we will try our best to negotiate a fair deal for you.

The Lower Score The Higher Rate – This is How it Works When it Comes to Bad Credit Mortgage

Banks pretty much always turn down people with bad credit but some lenders are willing to give you a chance based on other information. Searching for such companies and lenders will be a long and time consuming process. Luckily, we can help you to get the best loan arrangement. After we assess your financial situation we will have a list of appropriate lenders for you right away.

The lower your credit score the higher the mortgage rate will be from the lender. If it is possible, then it is best to make a larger down payment first so that you have a greater chance of getting accepted and so that the rate goes down a bit. Our professional team at Adrianov Mortgage will assist you in the search and help filter out bad offers. We guarantee to get you the best rate that is possible. No matter how bad your credit score is, please contact us to figure out a solution together.

Featured Rates

starting from

5.75%| Term | Rate |

|---|---|

| HELOC | 4.45% (Prime rate) |

| Lender | Rate | Term |

|---|---|---|

| 3.99% | 5 year | |

| 4.09% | 4 year | |

| 3.89% | 3 year | |

| 3.89% | 2 year | |

| 4.19% | 1 year |

| Term | Rate |

|---|---|

| 5 year variable | 3.45% (Prime - 1.05%) |

| 3 year variable | 3.55% (Prime - 0.9%) |

| Term | Rate |

|---|---|

| Line of Credit | Starting at 7.2% |

| Equity Loans | Starting at 6.5% |

| Private Mortgages | Starting at 5.49% |

| Reverse Mortgages | Starting at 4.99% |

You have questions. We are here to help!

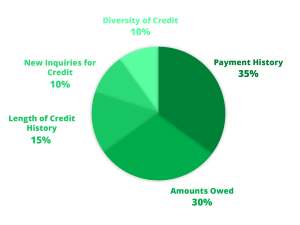

What Are The Factors That Affect Your Credit Score?

A credit score is usually a reflection of a credit report, and lenders use it to gauge your likelihood of paying back their money. The scores change regularly according to several factors that affect them. The factors include payment history, types of credit, credit history duration, and credit checks. The credit bureaus will use those factors to calculate the scores and adjust them accordingly. You should always take your credit score seriously and check it regularly to determine whether it’s improving or lowering, especially when you’re about to take a mortgage. Good practices such as using 30% or less of your credit limit can help you keep the score high.

Payment History (35%)

Your debt payment history is an essential factor for determining your credit score. The credit bureaus will look at how you have been paying your previous debts, except the mortgages, to figure out how you will pay them back. The bureaus will look for details such as deferred payments, whether the payments were made according to the debt agreement, and if the debt was paid in full or partially. Your history will also show if you paid the loan as a collection or filed for bankruptcy.

The number of scores you lose when you fail to make payments in time or meet any of the other conditions above remains unknown. However, the credit bureaus have made it known that if you start with a high score, your chances of losing them will be higher. If you have a low score, you won’t lose as many points when you don’t maintain good financial practices. For instance, if you have an 800 score, and you pay late the first month, you can drop over 100 points. On the other hand, if your score is 600, you won’t lose more than 80 points at the first late payment. Recent credit history is also more likely to influence the lender than an earlier one.

Amounts Owed (30%)

Your credit score will also depend on the current loans you owe. The more you owe, the more it becomes harder to keep up with payments, which increases the chances of defaulting and the score lowering. You may think that you can manage more loans if given, but statistics show otherwise. If you maximize your credit limits regularly, you won’t improve your score. That is why it is always advisable that you keep your credit utilization lower than 30%. Using over 60% of the limit regularly is unadvisable.

Larger loan amounts also pose a risk to lenders. They perceive it as your inability to keep up with all the payments at the same time. The risks increase when there is a possibility of losing your job. Always take loans that you can continue paying, even if you lose your main source of income.

Length of Credit History (15%)

This factor shows how long you have stayed with a loan. Lenders use this information to determine how you use the credit they give you and whether you’ll be responsible enough to maintain regular payment. Lenders tend to fear giving loans to people who haven’t used credit for a long time. It makes it harder for them to figure out if you are responsible. At the same time, too much credit within a short period may portray you as an irresponsible borrower. The best solution is to use minimal credit over a long duration.

Your credit history is usually cleared from the credit report after 7 years. In the meantime, the report will show when you get the credit, how you use it, and whether it is still active. Short credit history will result in a low credit score. A long and responsible credit use will get you a higher score. Pay attention to the debts you get into and how you use the money.

New Inquiries for Credit (10%)

Inquiring about new credit is usually a sign that you’re experiencing financial difficulties. The more frequently you apply for loans, the more you will be showing your lenders that you’re in a financial mess. They will inquire about you, and those inquiries usually show how many times your credit history has been checked. If lenders have looked into your credit score for the previous 5 years many times, or if you have opened many credit accounts recently, it will reflect on your credit score.

The duration you take before opening a new credit account and the time-lapse since your last credit inquiry will also play a role in your credit rating. They show whether you’re building a new credit history since your last payment completion. Getting a new loan also adds to your debts, which makes the payment more difficult. These are some of the common factors for low credit ratings.

Diversity of Credit (10%)

Credit diversity can impact your credit score positively or negatively. If all the other essential factors affecting the score are positive, multiple credits won’t reduce the rating. If not, too many loans will damage your credit rating.

Using different credit products properly can show your lender that you’re responsible. For instance, if you can prove that you have paid all your lines of credit and credit cards in full and on time, the lender will trust you with their money. In most cases, diversity of credit contributes to your credit score automatically. If you want a higher score, you will have to manage your funds properly and apply for one credit at a time.

How To Fix Bad Credit?

Fixing a bad credit score means changing all the factors that contribute to that score. The first step will be to identify what is causing the score to reduce. Figure out whether your bad credit is because of irresponsible expenditure or loan defaults, then start working on changing it. Once you understand the root cause of the problem, you will also know how to avoid a recurrence of it.

You can always fix bad credit by changing your financial management habits. Start by paying bills on time, monitoring the score, disputing discrepancies, and waiting for the 7 years credit report timeline to elapse. If you can’t manage these, several programs that can help you out are available. Our bad credit mortgage brokers can help you select the most suitable program for your lifestyle.

Check Your Credit Score

You can find all the information about your credit score on your credit report. The report is available on Equifax or Transunion online platforms. These are the major credit bureaus in Canada, and they can give you all the information you need about your credit.

Checking your credit score won’t result in a negative review the way it does when someone else does it. The steps included in the report will guide you as you go through it. When you’re done, you can ask the credit bureaus for your credit score.

Check all the reports to ascertain that information matches how you’ve handled your finances. Confirm that the reports reflect the exact number of accounts you have open, the ones you’ve closed, and the times you’ve made timely payments in full. Some banks may make an error when reporting your account details and activities. That is why you must pay attention to the dates, names, and transaction amounts.

Pay Down Your Debts And Bills

Always pay your bills and monthly debts in time to show that you have your finances under control. In most cases, companies handling your utility bills won’t report them to the credit bureau. However, if you make a habit of not paying on time, or you have several bills pending, the companies will send over collectors, and that will reflect on your credit report. Unlike utility bills, your credit card bills usually appear on the credit reports whether you pay them or not. As such, you should strive to pay them before expiry to prevent your score from reducing. Try to take care of your larger debts as well, even if it means getting another mortgage to consolidate them. Avoid debts that could land you in court or result in your property being seized as collateral.

Avoid Opening Too Many New Accounts

Having several credit accounts can be beneficial to your credit history, but it could also land you in trouble with the credit score. The more applications you make, the more lenders will check your credit report or request your score. This process is known as a hard inquiry, and it can impact your credit report negatively.

A hard inquiry differs from a soft inquiry, which is done for non-credit purposes, such as employment reasons. A hard inquiry can remain on your report for up to 6 years. During that time, your potential lenders will use it to decide whether you are reliable enough to get a loan or not. The best way to avoid hard inquiries is by limiting your accounts.

Dispute Errors On Your Credit Reports

Both banks and credit bureaus can make mistakes when compiling reports. That is why you should double-check your credit report for accuracy. In case you find any inconsistencies, contact your creditor immediately and ask them to correct the mistakes. If they don’t, contact the reporting agency and file a dispute with them. Make sure you file your complaint with the company that gives you the report. The agencies often allow clients to explain their problems, especially when there is a matter of contention. You have to be careful with your dispute because negative information on your credit can stay there for 7 years.

What Should I Consider When Applying For A Mortgage With Bad Credit

The process of applying for a mortgage can overwhelm you, especially if it's your first time. You may be tempted to reveal too much information or share documents that the lender doesn’t need in a bid to impress them. However, it's better to stick to what the lender requires and supply the documents that the lender needs only. Different lenders will ask for different documents, depending on the type of loan you want, your financial status, and your credit rating. Adrianov Mortgage brokers can help you analyze the necessary documents for the type of mortgage you want, including bad credit mortgage, to ensure the lender gets them as soon as possible. In case a lender wants extra documents, they will go through your bad credit mortgage broker, who will then ask you.

You must always protect all your documents because you will need them in the future, and they contain private information that shouldn’t fall into the wrong hands. Never give a mortgage lender original copies of whatever they ask for. Instead, make several copies of the forms for backup and keep the originals.

At Adrianov Mortgage, we have the best mortgage options for low and high credit scores alike. We are available to help you differentiate the various documents necessary for mortgage applications, to ensure you don’t give too much information away.

FAQ

How long does it take obtain mortgage approval if you have bad credit?

The duration for getting a mortgage with bad credit differs depending on the lender and the mortgage type. Some will take as little as one day, while others will take 48 hours or more. Our relationship with multiple lenders makes it possible to get approval within a duration that suits your needs.

How long does it take to fix bad credit in Canada?

The period it takes to repair bad credit will depend on the issues highlighted in your report. Those issues will determine the rectification measures you take and how long before those measures become effective. For example, if your bad credit score is because of a bad report, it could take up to 7 years before you get a chance to rectify it. However, if it is because of other reasons like delayed payments, paying the debts on time could improve the score within months. Our brokers can suggest the right programs to help you if you can’t fix the bad credit on your own.

Can I qualify for a mortgage with bad credit?

Yes, you can get a mortgage even if your credit is bad, but it won’t be easy, especially if you want to borrow from banks. A bad credit mortgage broker from Adrianov Mortgage brokers can help you get an alternative borrowing source. Some of the lenders we work with don’t do credit checks, which means that you can get a mortgage regardless of your credit situation. Talk to our attentive brokers, and let us find ideal solutions for you. With us, you will get any mortgage amount, including 80% of your property value, for second mortgage loans or refinancing.

Where to get a mortgage with bad credit?

Traditional lenders don’t usually give mortgages to people with bad credit records or poor ratings. That means private lenders are the best people to approach when you need a bad credit mortgage. Adrianov Mortgage brokers are the best partners to work with if you need a private mortgage lender, but your credit rating is below fair. We won’t let your bad luck affect your future, and we won’t limit your options either. When it comes to our clients, we don’t hold anything back.

Google Reviews

Was looking for a mortgage broker in Toronto. Heard about Leon and his team from a co worker and decided to give them a call. after some time on the phone talking about mortgages and what would work best for me I was VERY impressed. They were polite and most importantly they knew what they were talking about. We then scheduled an appointment and I got my mortgage with a great rate. Definitely recommend.

Got tired of sow service and mediocre rates from my bank, so I started looking for a mortgage broker. Had some family friends recommended Leon and his team, so decided to check them out. Was very impressed with Leon, he guided me through step by step, recommended a mortgage and I ended up switching to him. My rate is better and he always answers call and emails right away.

A little while back my wife and I finally decided to stop renting and get a place of our own. After some searching we found a condo we both liked and that was in our price range. The next step was a mortgage, but honestly, neither of us knew too much of what we were getting into. We found Leon and his team after a quick search on google and have had a wonderful experience. Leon and his team of mortgage brokers are VERY knowledgable, polite, work fast and just all around very professional. They answered all our questions and we got a great rate.

Getting a private mortgage was not easy to be honest, but at least with Mr. Leon it was doable. Thank you for your help!

Going through with this company was my best decision. These Burlington mortgage brokers are real professionals. They helped me to save thousands of dollars, I'm not sure I'd find such a good offer myself.

Contact Us

Adrianov Mortgage Across Ontario

…by providing award winning customer service to each and every single client.