FIVE STAR CUSTOMER SERVICE!

FIVE STAR CUSTOMER SERVICE!  +1 866 921 8890

+1 866 921 8890

This can have a major effect on your interest rate and how much you will ultimately have to cough up for your home. As such, knowing how mortgage lenders establish your creditworthiness and risk profile can help you get a clearer picture of what your mortgage will look like and avoid nasty surprises.

Mortgage Offers

...pick the one thats right for you.

$1000 Cash Back or Free iPad

When You Close With Us!

Featured Rates

starting from

5.75%| Term | Rate |

|---|---|

| HELOC | 4.45% (Prime rate) |

| Lender | Rate | Term |

|---|---|---|

| 3.79% | 5 year | |

| 3.99% | 4 year | |

| 3.59% | 3 year | |

| 4.29% | 2 year | |

| 4.19% | 1 year |

| Term | Rate |

|---|---|

| 5 year variable | 3.44% (Prime - 1.01%) |

| 3 year variable | 3.65% (Prime - 0.8%) |

| Term | Rate |

|---|---|

| Line of Credit | Starting at 7.2% |

| Equity Loans | Starting at 6.5% |

| Private Mortgages | Starting at 5.49% |

| Reverse Mortgages | Starting at 6.29% |

You have question. We are here to help!

Housing expenses vs income ratio

This is one of the most basic factors lenders take into account to determine how capable you are of repaying your loan or mortgage. It’s generally recommended that no more of 30% of your gross income (after taxes) should go to your housing costs. These costs include either your mortgage (or rent), your property tax, and your home insurance.

Most Canadian lenders maintain a maximum 28% of housing expenses to income requirement. This can vary between individual lenders as well as your personal circumstance. A very good credit score can offset this amount slightly. The 50/20/30 rule, where 50% of your income goes to fixed monthly expenses (housing, debit orders, etc.), 20% goes to variable monthly expenses (groceries and entertainment), and 30% goes to savings, is considered to be a good profile.

Debt-To-Income ratio (DTI)

Some people may have more than one big loan they are paying off at any one time. It could be various mortgages, a loan for a business venture, student loans or a loan for that fancy new car of yours.

Any lender will pay close attention to your accumulated debt and measure this against your income to determine whether you can take on more debt. If you know you might need a mortgage, it might be best to hold off on any big loans until that time. It might also help to try and break some of your loans early.

Most lenders will require that your housing expenses we talked about previously and your monthly repayments together come to no more than 36%. That means you only have another 8% of debt-wriggle-room on top of your housing expenses.

Available capital

The initial down payment you make no doubt has a big influence on the bottom-line of your mortgage. Cutting 20% off the top of your principal puts a big dent in the amount of interest you will need to pay. So, having this kind of money available is obviously a big plus.

If you have made some solid investments and have a good and diverse portfolio, it also lessens the risk you are at to fail to make your payments.

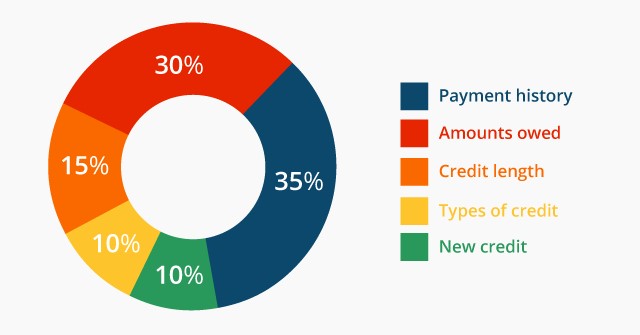

Credit history

There are a few factors that lenders consider here:

- Credit score: – Your overall credit score is obviously one of the most important factors that give many sleepless nights. 750 plus is considered an excellent score that will get you the best rates. 680 will qualify you according to most lenders whilst a score of 600 or less disqualifies you from almost any traditional financial institution.

- Credit mix: – This is the type of things or reasons for why you have purchased on credit before. This could help them establish how likely you are to go into more debt or how responsible you are.

- Credit history: Obviously, the longer your credit history is, the clearer picture a lender can get of you and gives them an idea of your consistency at repaying debt.

Google Reviews

Was looking for a mortgage broker in Toronto. Heard about Leon and his team from a co worker and decided to give them a call. after some time on the phone talking about mortgages and what would work best for me I was VERY impressed. They were polite and most importantly they knew what they were talking about. We then scheduled an appointment and I got my mortgage with a great rate. Definitely recommend.

Got tired of sow service and mediocre rates from my bank, so I started looking for a mortgage broker. Had some family friends recommended Leon and his team, so decided to check them out. Was very impressed with Leon, he guided me through step by step, recommended a mortgage and I ended up switching to him. My rate is better and he always answers call and emails right away.

A little while back my wife and I finally decided to stop renting and get a place of our own. After some searching we found a condo we both liked and that was in our price range. The next step was a mortgage, but honestly, neither of us knew too much of what we were getting into. We found Leon and his team after a quick search on google and have had a wonderful experience. Leon and his team of mortgage brokers are VERY knowledgable, polite, work fast and just all around very professional. They answered all our questions and we got a great rate.

Getting a private mortgage was not easy to be honest, but at least with Mr. Leon it was doable. Thank you for your help!

Going through with this company was my best decision. These Burlington mortgage brokers are real professionals. They helped me to save thousands of dollars, I'm not sure I'd find such a good offer myself.

Contact Us

Adrianov Mortgage Across Ontario

…by providing award winning customer service to each and every single client.